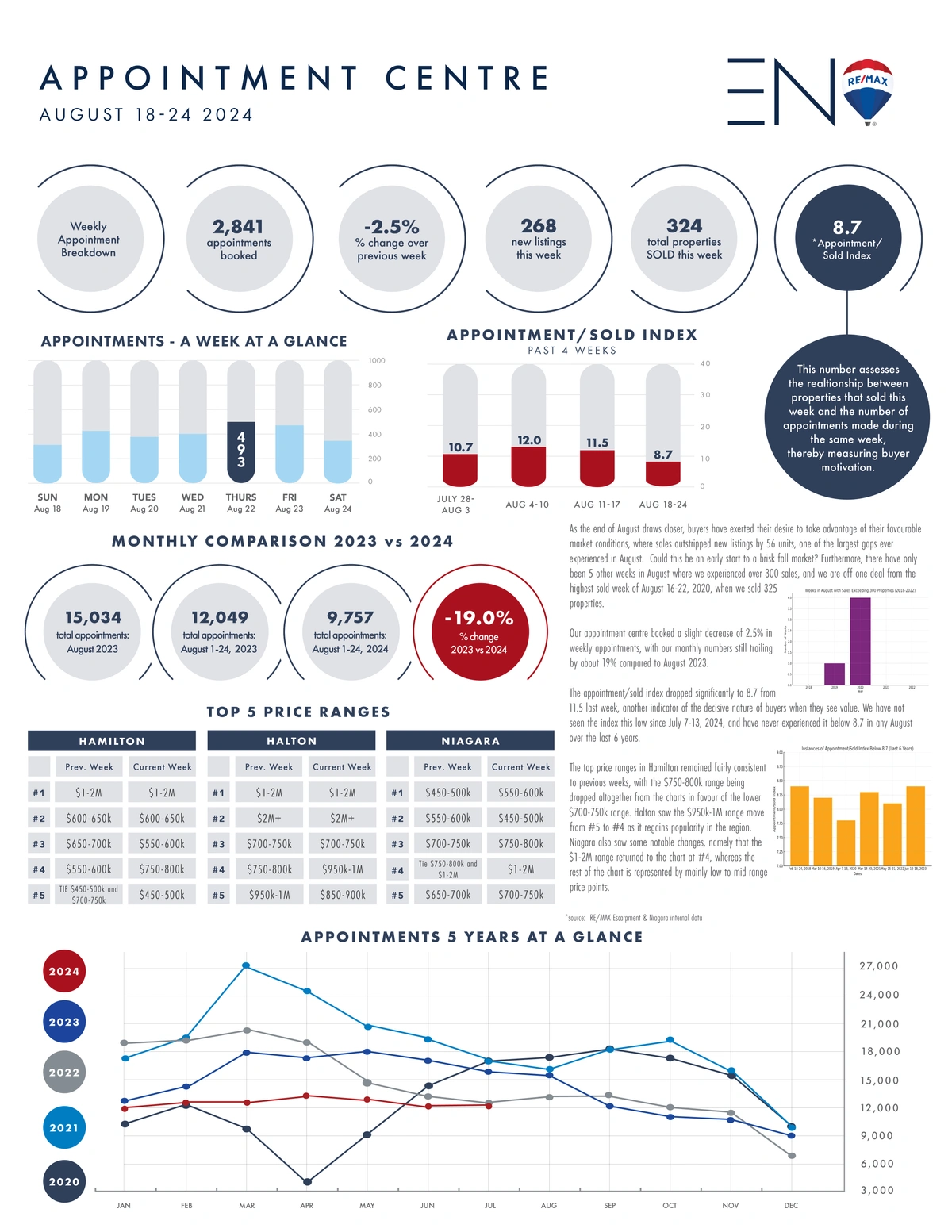

As the end of August draws closer, buyers have exerted their desire to take advantage of their favourable market conditions, where sales outstripped new listings by 56 units, one of the largest gaps ever experienced in August. Could this be an early start to a brisk fall market? Furthermore, there have only been 5 other weeks in August where we experienced over 300 sales, and we are off one deal from the highest sold week of August 16-22, 2020, when we sold 325 properties.

Our appointment centre booked a slight decrease of 2.5% in weekly appointments, with our monthly numbers still trailing by about 19% compared to August 2023.

The appointment/sold index dropped significantly to 8.7 from 11.5 last week, another indicator of the decisive nature of buyers when they see value. We have not seen the index this low since July 7-13, 2024, and have never experienced it below 8.7 in any August over the last 6 years.

The top price ranges in Hamilton remained fairly consistent to previous weeks, with the $750-800k range being dropped altogether from the charts in favour of the lower $700-750k range. Halton saw the $950k-1M range move from #5 to #4 as it regains popularity in the region. Niagara also saw some notable changes, namely that the $1-2M range returned to the chart at #4, whereas the rest of the chart is represented by mainly low to mid range price points.