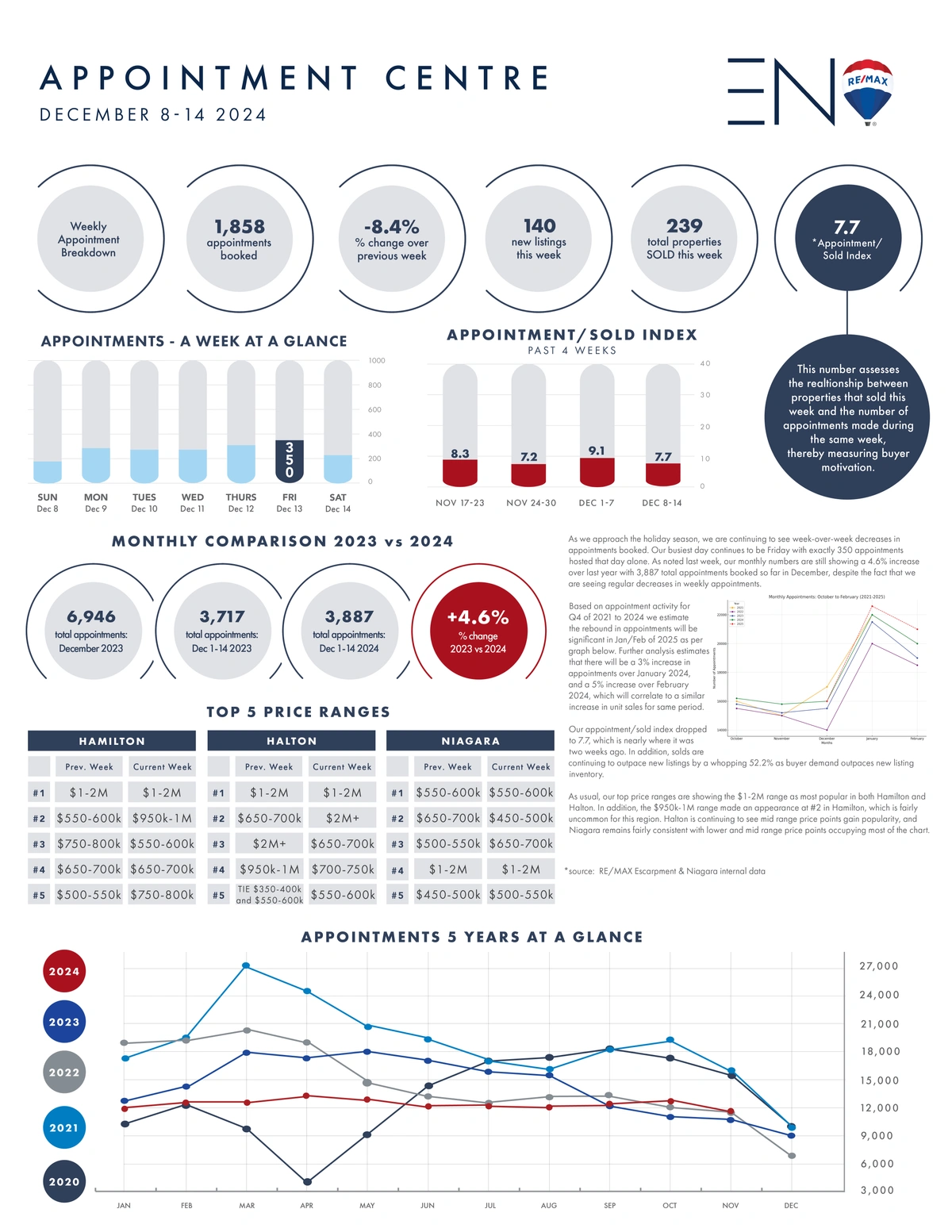

As we approach the holiday season, we are continuing to see week-over-week decreases in appointments booked. Our busiest day continues to be Friday with exactly 350 appointments hosted that day alone. As noted last week, our monthly numbers are still showing a 4.6% increase over last year with 3,887 total appointments booked so far in December, despite the fact that we are seeing regular decreases in weekly appointments.

Based on appointment activity for Q4 of 2021 to 2024 we estimate the rebound in appointments will be significant in Jan/Feb of 2025 as per graph below. Further analysis estimates that there will be a 3% increase in appointments over January 2024, and a 5% increase over February 2024, which will correlate to a similar increase in unit sales for same period.

Our appointment/sold index dropped to 7.7, which is nearly where it was two weeks ago. In addition, solds are continuing to outpace new listings by a whopping 52.2% as buyer demand outpaces new listing inventory.

As usual, our top price ranges are showing the $1-2M range as most popular in both Hamilton and Halton. In addition, the $950k-1M range made an appearance at #2 in Hamilton, which is fairly uncommon for this region. Halton is continuing to see mid range price points gain popularity, and Niagara remains fairly consistent with lower and mid range price points occupying most of the chart.