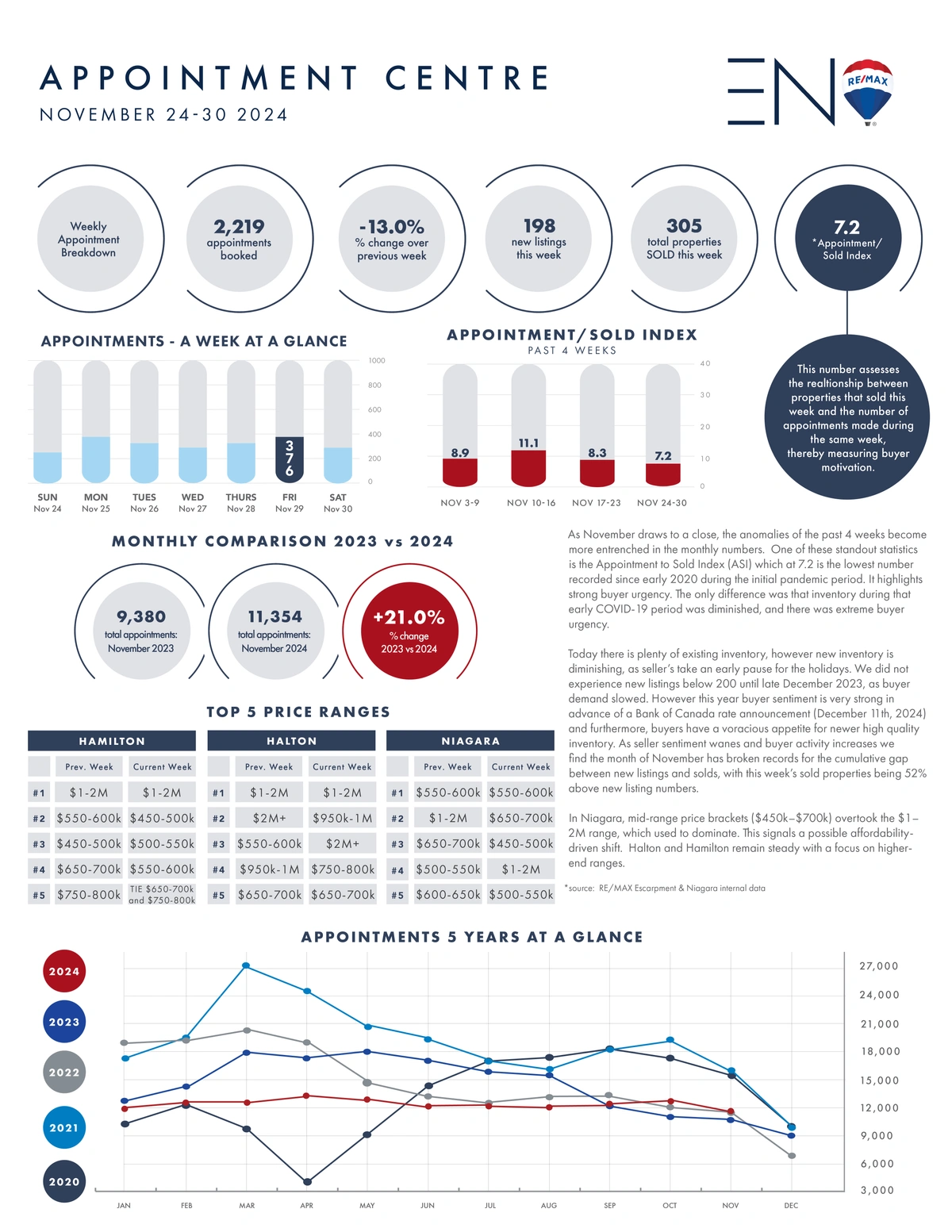

As November draws to a close, the anomalies of the past 4 weeks become more entrenched in the monthly numbers. One of these standout statistics is the Appointment to Sold Index (ASI) which at 7.2 is the lowest number recorded since early 2020 during the initial pandemic period. It highlights strong buyer urgency. The only difference was that inventory during that early COVID-19 period was diminished, and there was extreme buyer urgency.

Today there is plenty of existing inventory, however new inventory is diminishing, as seller’s take an early pause for the holidays. We did not experience new listings below 200 until late December 2023, as buyer demand slowed. However this year buyer sentiment is very strong in advance of a Bank of Canada rate announcement (December 11th, 2024) and furthermore, buyers have a voracious appetite for newer high quality inventory. As seller sentiment wanes and buyer activity increases we find the month of November has broken records for the cumulative gap between new listings and solds, with this week’s sold properties being 52% above new listing numbers.

In Niagara, mid-range price brackets ($450k–$700k) overtook the $1–2M range, which used to dominate. This signals a possible affordability-driven shift. Halton and Hamilton remain steady with a focus on higher-end ranges.